Nvidia (NASDAQ:NVDA) has once again delivered the goods. The AI chip giant’s third-quarter results showed that the AI opportunity remains ample.

Don’t miss our Black Friday offers:

Revenue for the October quarter reached $35.08 billion, up 93.6% year-on-year, beating analyst expectations by $1.95 billion. Of that, data center revenue (the division that includes Nvidia’s AI chips) accounted for $30.8 billion, up 112% year over year. This strong growth was driven by demand for the company’s Hopper computing platform, which supports training and inference for large-scale language models, recommendation systems, and generative AI apps.

adjective. Gross profit margin reached 75%, meeting street expectations. EPS of $0.81 beat estimates by $0.06.

As always, the outlook was strong. For the fourth quarter (January quarter), the company expects sales to be $37.5 billion (plus or minus 2%). The Street was asking for just $37.1 billion.

“The era of AI is in full swing,” CEO Jensen Huang said, adding, “AI is transforming every industry, business, and country.”

NVDA has certainly changed the lives of many NVDA investors, considering the stock price has nearly tripled since the beginning of the year, not to mention the huge strides it has made over the past few years.

Rosenblatt analyst Hans Mosesmann, who ranks among the top five Wall Street analysts in predicting stocks, called the results a “solid beat and rally.” “Hopper demand is higher than expected,” he said, adding that Nvidia’s Blackwell supply growth is “more than expected (sold out in the next few quarters).”

“Net/Net,” Mosesman continued. 1) Quarterly and outlook met. 2) Blackwell’s demand profile is positive heading into 2025. 3) Speculation of ‘power’ issues plaguing new lamps dismissed, short-term networking air pockets, gaming constraints (this is where AMD benefits), and GM’s trajectory back to the mid-70s in a few quarters. ”

To this end, Mosesman rates NVDA stock a “buy” while raising his price target to a high of $220, suggesting the stock could rise an additional 50% over the next 12 months. There is. (Click here to see Moses Mann’s track record)

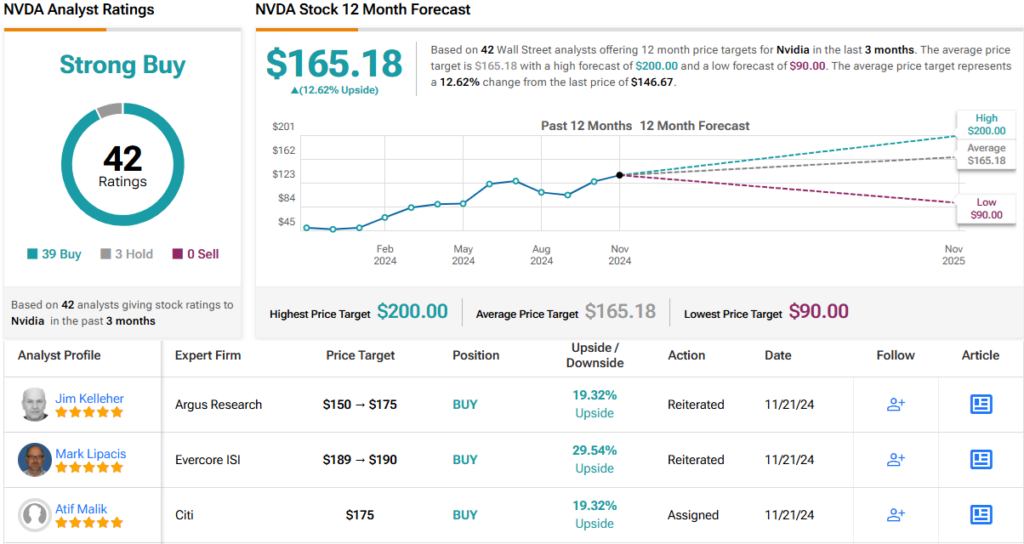

Overall, Nvidia’s success story has many believers. 39 out of 42 analysts recommend the stock to buy, and only 3 say “hold,” giving the consensus rating a “strong buy.” The average price target of $165.18 implies ~13% upside, but Mosesman clearly thinks Nvidia still has room to run. (See NVDA stock price prediction)

To find good ideas for trading stocks at attractive valuations, visit TipRanks’ Best Stocks to Buy, the tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. Content is for informational purposes only. It is very important to perform your own analysis before making any investment.