remains a long-term winner despite the noise")

Nvidia (NVDA), an artificial intelligence (AI) genius with the third highest market capitalization in the world, saw its market capitalization drop significantly following its second quarter results in late August. However, NVDA stock is showing momentum again, rising 5% last week. After briefly passing the $3 trillion milestone earlier this year, investors are wondering what the future holds. My theory remains the same. I’m bullish on NVDA stock as an investment because of its clear AI advantage and exponential growth potential.

NVDA’s long-term AI-driven growth trajectory remains in place

With blue-chip clients like Microsoft (MSFT), Alphabet (GOOGL), Meta (META), and Amazon (AMZN) ramping up their AI efforts, NVDA is well positioned for a long growth runway. known. But beyond these major customers, NVIDIA’s AI adoption is still rising across all industries, increasing my optimism for NVDA stock. Companies across industries and geographies are keen to incorporate the benefits of AI into their operations. Similarly, NVDA continues to collaborate with top companies.

There’s a reason AI-minded companies flock to NVDA. NVDA is not only the leader in AI GPU processors, but also provides a complete end-to-end AI infrastructure that dramatically increases productivity. This is something few, if any, of our global AI competitors can achieve.

NVDA continues to be a leading one-stop AI company and profits are growing

Another reason I’m optimistic about NVDA is CEO Jensen Huang’s relentless focus. He is committed to transforming NVDA into a fully AI-driven data center powerhouse, covering all aspects of hardware and software under the NVDA brand.

This strategy is the main reason why NVDA is able to maintain premium prices for its products and contributes to steady growth in profit margins. But critics argue that NVDA’s extraordinary revenue and profit growth may not be sustainable. Some members of the investment community are concerned about slowing revenue growth in the coming years.

For context, NVDA reported an impressive 217% increase in data center revenue for fiscal year 2024. While that growth is expected to slow to around 130% in 2025, this is still an impressive triple-digit number, especially considering the strong baseline of FY2024 for comparison. . Although lower than today’s pace, these are still notable growth projections for the future. I see analysts’ bullish forecasts as a reason to remain confident in this AI leader, especially as the disruptive potential of generative AI is just beginning to become clear.

Demand for NVDA’s chips is strong, which should drive future revenue growth in the coming quarters. Therefore, despite some investor concerns, I expect NVDA to continue to maintain its clear AI advantage with an unbeatable competitive moat and best-in-class AI products and services.

A discussion of Nvidia’s impressive quarterly earnings.

Nvidia announced yet another impressive second quarter results on August 28, 2024, driven by continued momentum in accelerated computing and generative AI. Adjusted earnings were $0.68 per share, well above the analyst consensus estimate of $0.65 per share. This number was significantly higher than the $0.27 per share in Q2 2023 (+152%).

The company posted 122% year-on-year revenue growth for the three months ended July 31, reaching $30.04 billion, beating analyst expectations. Importantly, revenue from the company’s fine jewelry division, Data Center, rose 154% year-over-year to $26.3 billion. Additionally, NVDA’s adjusted gross margin expanded 5 percentage points to 75.1% from 70.1% a year ago. The stock fell slightly following the second-quarter report, as many investors were clearly expecting even bigger numbers. The stock continued its downward trend after that, bottoming out just above the $100 level on September 6th.

Nvidia’s third-quarter guidance was less encouraging for investors, with revenue expected to reach about $32.5 billion. Guidance was lower than expected. Adjusted gross margin is expected to be flat at approximately 75%, compared to 75.15% in the second quarter.

NVDA insider selling concerns are over

Nvidia insider selling has put downward pressure on NVDA stock in recent months. Please note that CEO Jensen Huang sold NVDA stock in multiple transactions between June and September, but these sales were part of a pre-trading plan adopted in March. is important. The plan allowed Huang to sell up to 6 million NVDA shares by the end of the first quarter of 2025.

Notably, Mr. Huang completed the sale of over $700 million worth of NVDA stock. Despite the importance of these sales, he remains the company’s largest individual shareholder. According to company filings, at last report Mr. Hwang held 786 million shares through various trusts and partnerships and 75.3 million shares directly. In total, Mr. Huang controls approximately 3.5% of the company’s stock, totaling approximately 859 million shares.

Considering its earnings growth potential, NVDA’s valuation is not high.

Investors may have been hesitant to purchase NVDA stock at current levels due to the company’s abnormal price rise and concerns about the company’s slowing growth.

But on the contrary, my argument is that NVDA stock isn’t as expensive as you might think. Currently, the expected PER is trending at approximately 43 times (based on FY2025 earnings forecast). This is actually a discount to the valuation multiples of its peers. For example, NVDA’s closest competitor, Advanced Micro Devices, a US-based semiconductor company, has a forward P/E ratio of 46.8x. Interestingly, NVDA’s current valuation still reflects a 10% discount to its five-year average forward P/E of 47.3x.

Given NVDA’s consistent outperformance and strong growth potential, its current valuation seems reasonable and justified. In my opinion, any future decline in the stock price could be a solid buying opportunity, especially considering Nvidia’s immense potential in the rapidly expanding AI market.

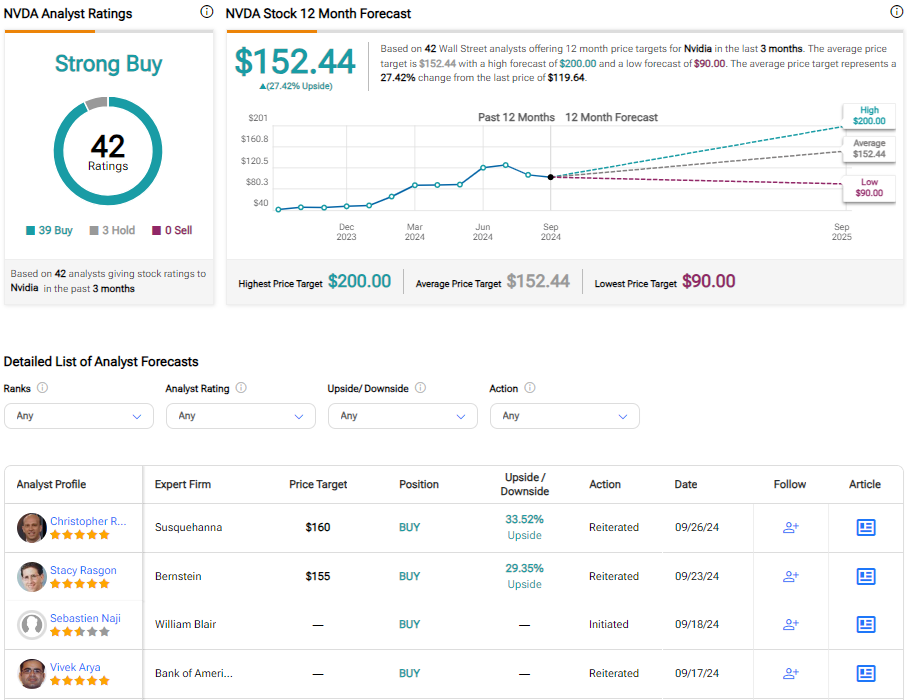

Is NVDA stock a buy or sell, according to analysts?

The TipRanks consensus rating is a Strong Buy, with 39 Buy ratings and 3 Hold ratings from analysts over the past three months. Nvidia’s average price target of $152.44 suggests potential upside of about 26% next year.

Bottom line: Consider NVDA stock for its long-term AI potential

Despite the recent weakness, NVDA stock has nearly tripled over the past year compared to the Nasdaq 100’s gain of about 37%. In my view, the post-earnings decline in NVDA stock was primarily due to profit-taking. After bottoming out around $100, the stock now appears to be in recovery mode.

In the short term, we believe the stock is likely to remain range-bound due to continued economic and political uncertainty. However, I view the decline as a buying opportunity. We believe NVDA is a strong long-term investment given the continued huge potential of AI.

Read the full disclosure