One of the biggest complaints from growth investors is that they need more growth candidates with reasonable valuations, which is rare when companies are doing well.

Still, you You can often buy stocks at a fair price when the market no longer finds them attractive. This is due to temporary weakness in end markets, as appears to be the case for ON Semiconductor. (Nasdaq: ON)This stock deserves attention from growth-oriented investors for three reasons.

A long-term growth story

The investment rationale for this stock hinges on management’s shift to the automotive and industrial end markets. ON Semiconductor’s intelligent technology is used in electric vehicles (EVs) and hybrid electric vehicles (HEVs), helping to reduce vehicle weight, extend driving range, and shorten charging times.

Meanwhile, the company’s advanced sensing technology is becoming a staple in smart factories and facilities, as well as in the automotive industry for advanced driver assistance systems (ADAS) and autonomous driving systems, and management continues to position the company for long-term growth in these end markets.

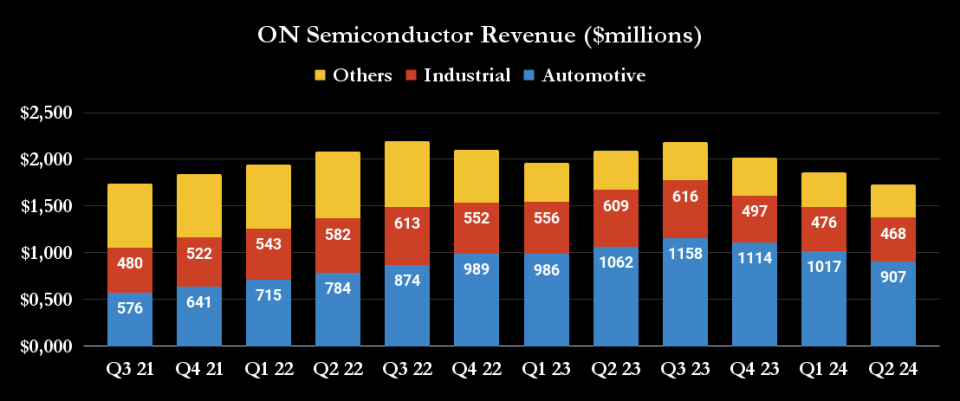

The slowdown is temporary

It’s fair to say that none of these end markets are thriving in 2024, at least not as strongly as they were expected to be coming into the year. Relatively high interest rates have slowed EV sales and caused automakers to cut development costs. The same is true for the industrial sector, where orders for industrial automation have slowed significantly.

The chart below illustrates the nature of the decline in the major industrial and automotive end markets.

However, the reason for the decline in revenue appears to be temporary and related to the high interest rate market. As interest rates fall, EV/HEV sales should recover, leading to investment in expanding production. As an example of the auto industry’s commitment to EV investment, ON Semiconductor recently signed a multi-year contract with Volkswagen to become a major supplier of Power Box solutions.

Additionally, spending on factory automation is slowing, as evidenced by ordering patterns from companies involved with factory automation, such as Emerson Electric and Rockwell Automation. The combination of slowing growth and automation product distributors reducing inventory rather than placing new orders is likely temporary.

There’s a reason companies like Emerson Electric, Siemens and Honeywell have made automation a key focus of their growth plans: factory automation allows developed countries to cost-compete with lower-cost countries in manufacturing.

The story continues

Attractive evaluation

It’s a problem that can’t be ignored: ON Semiconductor’s revenue is declining and is expected to decline further in 2024. What’s more, CEO Hassan El Khoury has spoken of an “L-shaped” recovery, meaning a sharp decline followed by a slower, more gradual recovery.

The good news is that a conservative outlook is factored into the stock’s valuation.

To illustrate the company’s attractive valuation, let’s look at standard valuation multiples using Wall Street analyst consensus. These are excellent multiples for a growth stock that will pass through a revenue and earnings trough in 2024, showing that the market does not believe the Wall Street consensus. In the last case, EV is enterprise value (market capitalization plus net debt) divided by earnings before interest, taxes, depreciation, and amortization (EBITDA).

ON Semiconductor

2023

Estimated for 2024

Estimated for 2025

Estimated for 2026

Price Earnings Ratio

17.1 times

19.4 times

15.5 times

12x

Price/Free Cash Flow

91.7 times

22.1 times

15.1 times

12.6 times

EV/EBITDA

11.4 times

11.5 times

9.6 times

7.6 times

Data source: marketscreener.com, author’s analysis.

The market has reason to be skeptical of the numbers: No one can feel completely at ease with a company whose sales are falling, but if the market is wrong, there is a lot of potential for upside.

Stocks to buy?

If you believe the future of the automotive industry lies in EV/HEV, ADAS and autonomous driving systems rather than traditional internal combustion engines (ICE), then you can be sure the future is bright for ON Semiconductor, especially as EVs generate significantly more content per vehicle than ICE-powered cars.

Additionally, the stock will be attractive to those interested in the megatrends towards factory automation, renewable energy, and EV charging networks.

These industries won’t recover anytime soon, but the underlying drivers are in place: clean energy (e.g., EVs) and increased manufacturing productivity from automation investments.

Should you invest $1,000 in ON Semiconductor right now?

Before buying ON Semiconductor shares, consider the following:

The analyst team at Motley Fool Stock Advisor has identified 10 stocks that investors should buy right now, and ON Semiconductor is not among them. The 10 selected stocks have the potential to generate big gains over the next few years.

Consider when Nvidia created this list on April 15, 2005… if you had invested $1,000 at the time of our recommendation, you would have $722,320.!*

Stock Advisor offers investors an easy-to-follow blueprint for success, with portfolio construction guidance, regular updates from analysts and two new stock picks every month. Stock Advisor The service is More than 4 times First S&P 500 recovery since 2002*.

View 10 stocks »

*Stock Advisor returns as of September 16, 2024

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has invested in and recommends Emerson Electric and Volkswagen. The Motley Fool recommends ON Semiconductor and Volkswagen Ag. The Motley Fool has a disclosure policy.

The post 3 Reasons to Buy ON Semiconductor Stock Like There’s No Tomorrow was originally published by The Motley Fool